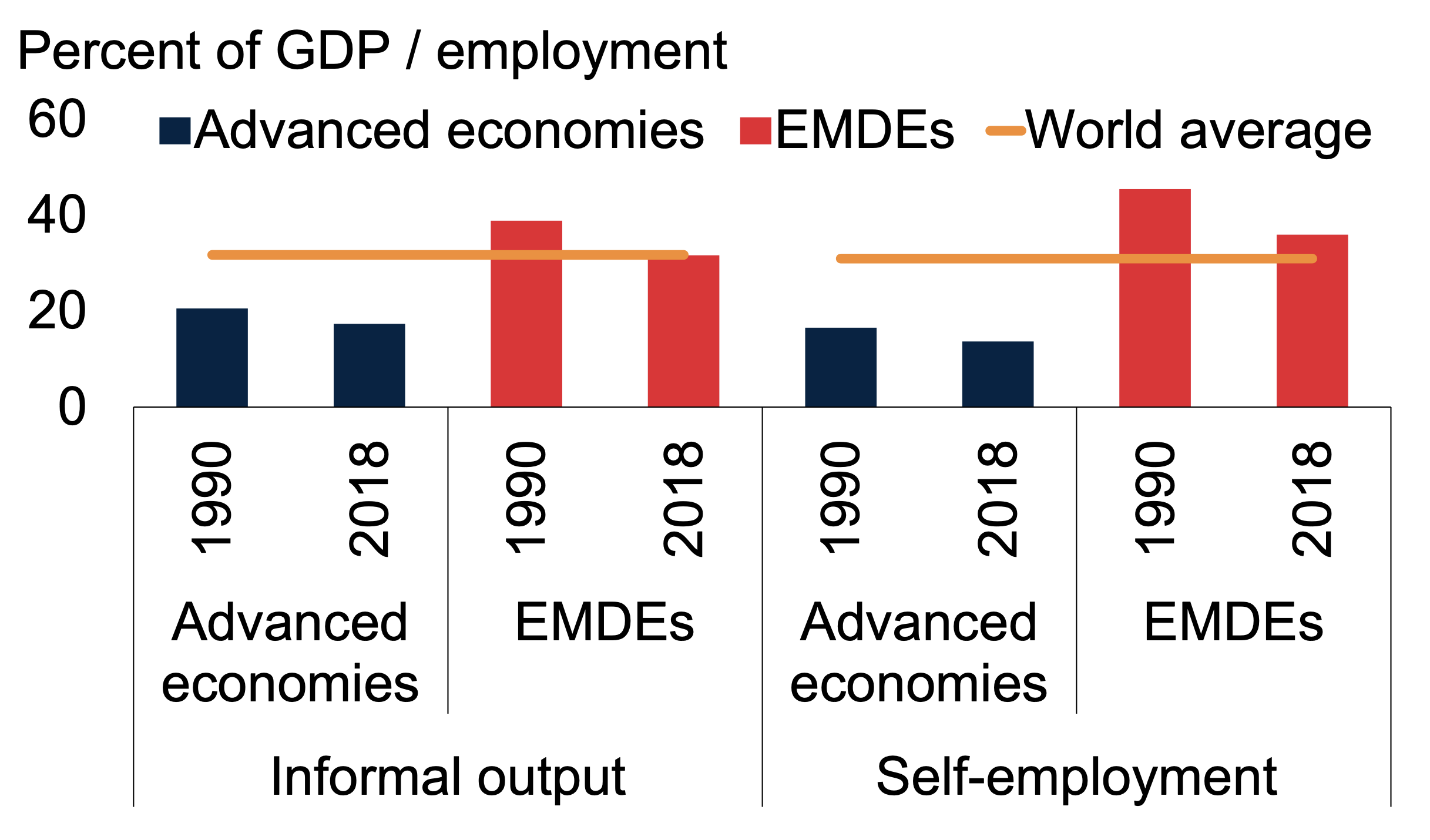

Informal economic activity is widespread around the world. On average, such activity accounts for about one-third of output, and informal employment captures almost one-third of total employment (Figure 1). It undermines revenue collections, stunts productivity, hinders investment, and traps some of the most vulnerable workers in low-paying, unproductive employment. For policymakers in countries with widespread informality, it is a formidable challenge.

Figure 1. Informality around the world

Sources: Elgin et al. (2021).

Note: Bars are simple averages. “EMDEs” stands for emerging marking and developing economies. Informal output is proxied by dynamic general equilibrium (DGE) model-based estimates in percent of official GDP. Self-employment, a common proxy for informal employment, is in percent of total employment. World averages between 1990-2018 are in orange.

Underdeveloped financial systems have often been identified as a potential cause of informality but the direction of causality has been difficult to pin down. Financial development can influence the benefits and costs of informal economic activity undertaken by firms and households. Firms in the informal sector are typically characterized by small scale, low capital-to-labor ratios, lack of investment, low productivity, a low propensity to implement new technologies, and unskilled managers. By influencing firms’ investment strategies, financial development promotes the transition of informal firms into the formal sector and, ultimately, encourages capital accumulation and productivity improvements.

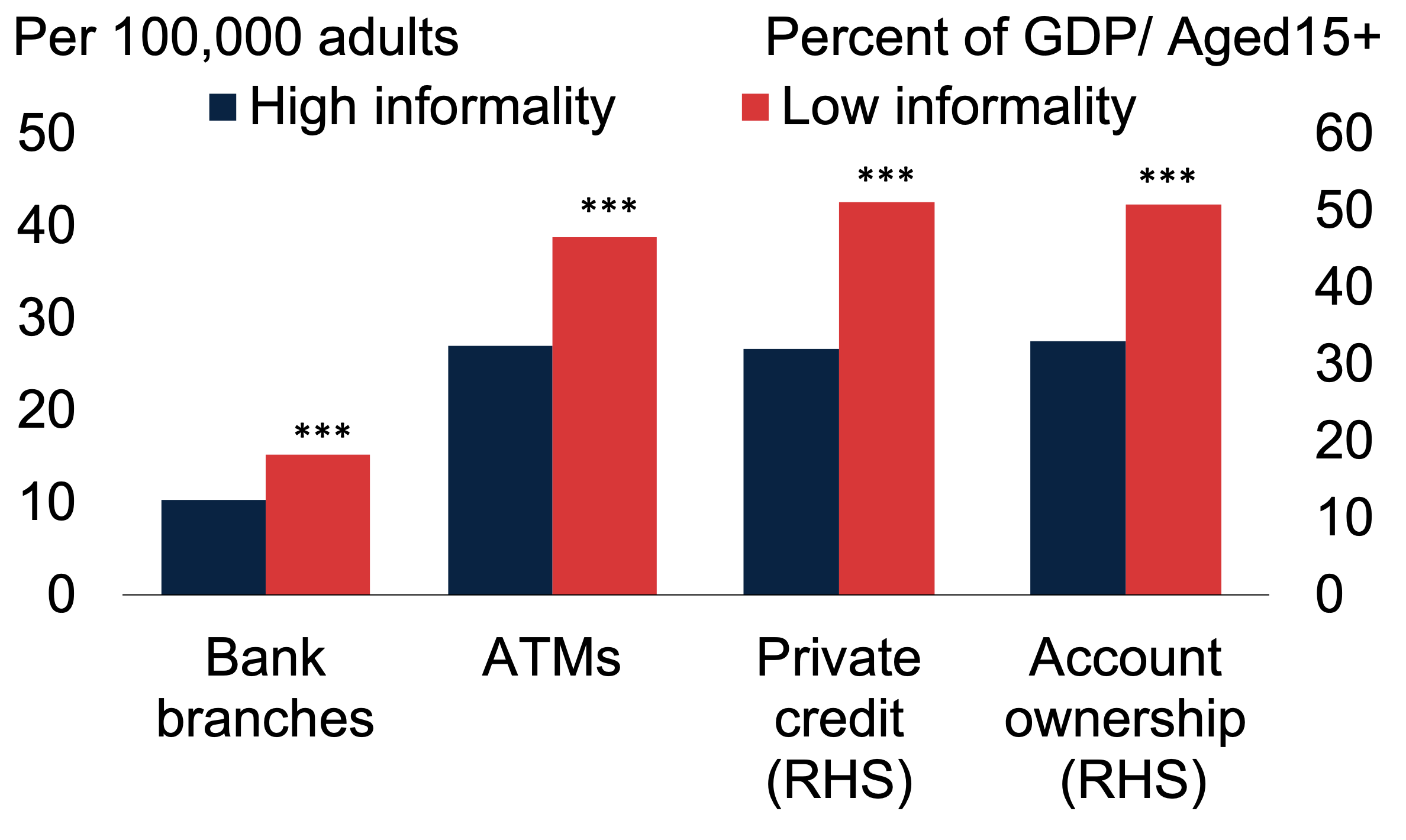

Plenty of empirical evidence shows that financial development is correlated with lower informality. Many empirical studies have found a robust and significant result, for different sets of countries, time periods, and definitions of financial development and informality, and controlling for numerous factors: Greater financial development is associated with less informality (Figure 2).

Figure 2. Financial development and informality

Sources: Ohnsorge and Yu (2022).

Sources: Ohnsorge and Yu (2022).

Note: Bars show simple averages for EMDEs over the period 2010-18. “High informality” (“Low informality”) are emerging market and developing economies (EMDEs) with above-median (below-median) dynamic general equilibrium (DGE)-based informal output measures. “Bank branches” measures the number of commercial bank branches per 100,000 adults. “ATMs” measures the number of automated teller machines (ATMs) per 100,000 adults. “Private credit” measures domestic credit to private sector in percent of GDP. “Account ownership” is the percentage of survey respondents (aged 15 and above) who report having an account (by themselves or together with someone else) at a bank or other financial institution, or report personally using a mobile money service in the past 12 months. *** indicates group differences are not zero at 10 percent significance level.

{kind=link}

No comment